ADM Q1 profits set for $50-60m hit caused by floods, cold weather

Agribusiness major Archer Daniels Midland said Monday that flooding across the US that has destroyed grain and oilseed stocks and swept away silos will reduce its pre-tax operating profit by up to $60 million this quarter.

The company – the ‘A’ in the so-called ABCD quartet of companies that dominate agribusiness alongside Bunge, Cargill and Louis Dreyfus – said the bulk of the hit would be shared equally between its carbohydrate solutions and origination businesses, which include corn trading and ethanol production.

“Rail transportation has been disrupted throughout the region; our corn processing complex in Columbus, Nebraska, was idled due to flooding and currently is running at reduced rates; and unfavourable river conditions since December are severely limiting barge transportation movements and port activities,” ADM said in a statement.

The US Midwest has suffered a severe winter as record-breaking cold weather that has hit corn processing volumes due to a slowdown in rail and truck transportation.

And earlier this month, heavy rains have meant widespread flooding across major corn and soybean growing areas and shut 10-17% of ethanol production capacity, according to various estimates.

“Taken together, we expect these severe weather disruptions to have a

negative pre-tax operating profit impact to ADM of $50 million to $60

million for the first quarter,” the company said.

Q1 operating profit for the carbohydrate solutions and origination business was $213 million and $45 million, respectively.

ADM is the first major agribusiness to outline the financial damage the floods will have.

Earlier on Monday, the USDA said it was assisting farmers in Iowa and other communities affected by the flooding.

The floods will likely hit corn plantings and boost soybean plantings, some analysts say.

AgriCensus Prices Over 500 daily Spot Marker and Forward Curve price assessments for wheat, corn, soy, barley, vegoils, meals and seeds.

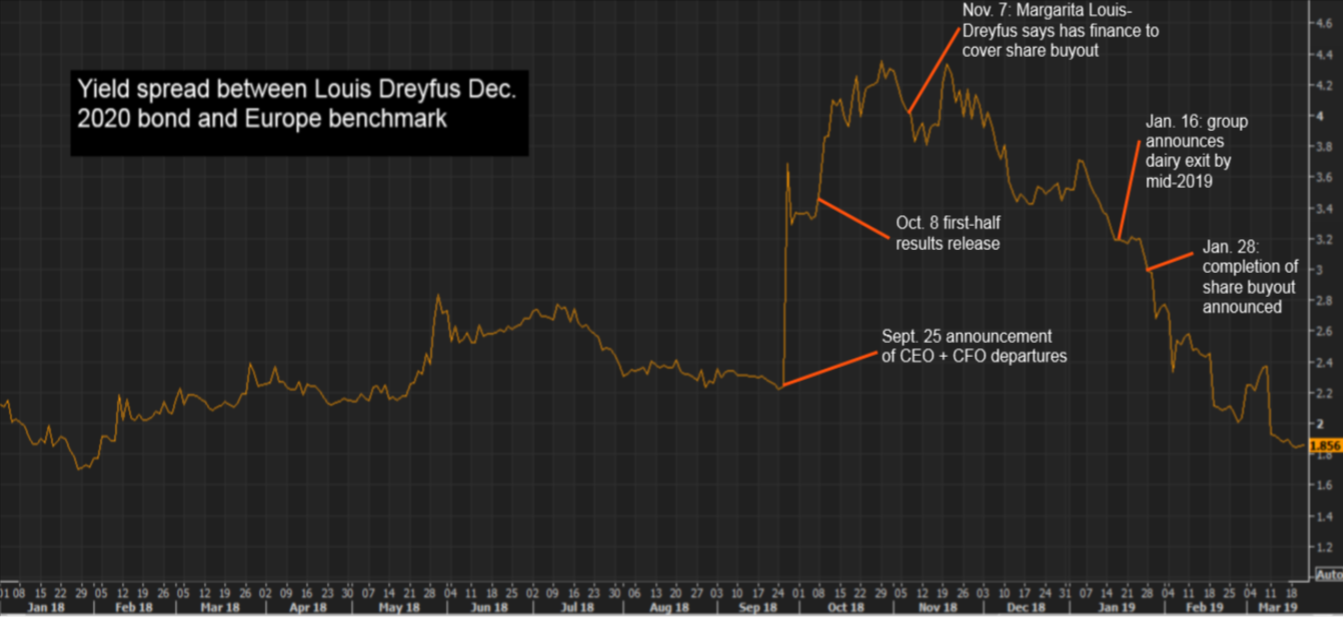

Louis Dreyfus Company is due later this week to publish their annual report and accounts for 2018. The company’s CEO told Reuters that year-to-date results had “significantly improved;” he suggested an upturn after a first half sapped by a soy price-hedging effect and emerging trade tensions. To put that in perspective, 2017 group net income was $225 million, excluding the now-sold metals business, close to 2015’s decade low of $211 million and well below a record $1 billion in 2012.

In the late 1970s, when he was researching his book, Merchants of Grain, Dan Morgan had considerable difficulty in obtaining any information from the “shadowy and unknown” grain trading companies. At that time they did not publish financial results.

With the exception of Cargill, they provided minimal assistance, or none at all, in the preparation of his book.

They had nothing against Dan Morgan; it was just the way things

were forty years ago. At that time a US Senator said of the grain

multinationals, “No one knows how they operate, what their profits

are, what they pay in taxes and what effect they have on foreign policy—or much

of anything else about them.”

In 1976 the French magazine L’Expansion, called Louis Dreyfus, “a commercial empire of which one knows nothing.” Pierre Louis-Dreyfus invited Dan Morgan to lunch in his private dining room. The fish with cream sauce was apparently superb, as was the wine, but the journalist left without learning anything of interest about the company.

Georges André, head of André & Cie—and the original “A” of the ABCD group of trading companies—invited Dan to “an excellent lunch of brook trout in a village restaurant,” but all he got out of it was some historical data. ADM—the new “A” in the ABCD group—was no more open. When Dwayne Andreas became CEO of the company in 1974, one of the first things he did was to eliminate a 27-person public relations department.

Dan

was granted a one-hour interview with Michel Fribourg, president of Continental

Grain, but later received a letter from Continental saying, “It has been decided that we choose not to

participate in further interviews with you.” The company had been in the grain business since the start of the

nineteenth century, had never published a company brochure.

None

of the trading houses were more obsessed with secrecy than Bunge. Dan Morgan

wrote that, “Bunge was a private company

about which nobody knew and nobody could speak…To Bunge officials public

relations meant keeping Bunge out of the limelight.”

But then the company’s controlling families had a particular reason for avoiding the limelight. Five years earlier, in September 1974 in Buenos Aires, the Montoneros—an Argentine youth movement—kidnapped Jorge and Juan Born, 40 and 39 years old respectively, the grandsons of the founding partner and heirs apparent of the company.

Juan Born was released six months later, in March 1975, and Jorge in June 1975. No details were even given as to the ransom paid for Juan, but the Montoneros claimed that the Bunge family had paid $60 million for the release of Jorge. Although that doesn’t sound like much now, it was a huge sum in 1975, equivalent at the time to one third of the annual Argentine defense budget.

It should come as no surprise that after the kidnapping, the family withdrew even further behind a veil of secrecy. Dan Morgan “did not get near the Hirschs or the Borns, the ruling families of the Bunge Company.” The closest he got was an hour-long interview with the president of Bunge’s North American division. After the meeting, Bunge’s public relations agent told him that he had “neither the time nor the inclination for further discussions.”

Compare Dan Morgan’s difficulties in obtaining information with the ease with which Daniel Ammann gained access to Marc Rich for his book, The King of Oil, published in 2010. Daniel wrote, “These oil and commodity traders…shared their thoughts and their memories with me, opened doors and documents, and explained the technicalities of trading and financing. They tried to show me the big picture, and they revealed their little secrets.”

But

then perhaps Mr Ammann was just lucky in his timing. Up until the series of

interviews that formed the backbone of his book, Marc Rich had systematically avoided

reporters and was, “considered the most

secretive trader of the notoriously furtive commodities trading community. For

years, no one had ever seen a photograph of him. The media had to resort to

artists’ sketches for their reports.”

Glencore, the successor company to Marc Rich, is now a public company, as too are ADM and Bunge. Cargill and Dreyfus are still privately owned, but both act as if they are publicly quoted; they publish detailed company reports and actively interact with the wider community, whether bond investors, clients, banks or journalists. COFCO, the new giant among the grain trading companies, is Chinese-government owned.

All of the large agricultural commodity companies are now active on social media, and actively engage with NGOs on issues related to environmental sustainability or human rights.

This

is a significant change since 1979, when Dan Morgan

wrote, “The companies…stay in the

shadows most of the time. Perhaps it was the ancient nightmare of the

middleman-merchant that made them all so secretive—the old fear that in moments

of scarcity or famine, the people would blame them for all their misfortunes,

march upon their granaries, drag them into the town square and confiscate their

stocks.”

Agricultural

merchants are still being dragged into the town square of public opinion, and they

are still regularly being blamed for varying misfortunes, but they are now very

much out of the shadows.

I

hope to publish my new book, “Out of the

Shadows: The New Merchants of Grain” this autumn.

The Presidents of Brazil and the US met this week to discuss the possibility of signing new trade deals, although experts noted that the trade between the two countries was already well-balanced. The US wants to expand ethanol exports but Brazil said it would only consider the move if it can export more sugar to the US, and few expect either side will make significant concessions.

The Brazilian President did mention the possibility of expanding trade relations with China. Having already invested USD 2 billion in Brazil’s agriculture, China is now interested in investing in the ethanol sector as the country prepares to meet its 2020 ethanol mandate. China absorbed 36% of Brazil’s agricultural exports and spent some USD 35 billion to buy Brazilian agricultural products in 2018, up 33% on year.

The EU and the US hit a roadblock during talks on a new trade agreement as the EU does not want to include agriculture. The EU did offer concessions, such as giving the US a share of its duty-free import quota of hormone-free beef, in an attempt to convince the White House to remove anti-dumping duties. Previous concessions included buying more soybean or classifying US soy as a sustainable biofuel feedstock. Australia and Uruguay – who took advantage of the beef quota when it was first opened in 2009 – could challenge this latest move at the WTO.

The US-China trade war was expected to have a long term impact on global agricultural tradeflows but the spread of the African swine fever outbreak in China could now counteract some of these changes. The crisis is helping US pig farmers as China imported huge amounts of pork over the past two weeks despite the 62% tariff recently imposed. However, the US is being very careful to protect its pig population from the virus and the USDA recently seized 450mt of contraband pork products from China, the largest seizure of contraband food in US history.

An expert suggested that the outbreak will continue to lower Chinese demand for soybean for years as feed demand will drop, although US soybean could be diverted to feed the pigs exported to China. Nonetheless, US soybean area will stay almost constant this year as farmers have no viable alternative – other grains such as sorghum and corn are also subject to Chinese duties. Farmers also hope the government will resolve the trade dispute or offer another aid package.

In Japan, Nestle announced that it will expand its range of KitKat ruby chocolates after a successful launch in 2018. Ruby chocolate was developed by Barry Callebaut and is supposed to be the fourth kind of chocolate – after dark, milk and white chocolate. The firm said it had been surprised by the speed and scale of social media reactions, which was more efficient than any marketing campaign. It added that chocolate trends were now made in Asia, as Asian tends to be more open to new foods. In the US, the biggest chocolate market, ruby chocolate still has not received government approval. Specialty ingredients makers, such as Denmark’s probiotic and enzyme maker Chr Hansen Holding and England’s Tate & Lyle, which makes non-sugar sweeteners and texturizers, are also expected to benefit from these new consumer trends.

ADM announced that it has agreed to purchase one of the biggest citrus ingredient maker in Europe, Ziegler Group. The firm recently purchased another citrus firm, Florida Chemicals, and highlighted that it was positioning itself to be a leader in the fast-growing citrus flavour sector.

Euromonitor warned that image recognition might start to drop as consumers switch to healthier food. For the moment, however, packaged foods remain very popular. Some 41 out of Euromonitor’s Top 100 Megabrands in 2019 were packaged food items, with Coca-Cola, Pepsi, Nescafe and Lay’s taking the first four positions of most valuable brands. An unexpected brand, Google, is making a foray into the food world by promoting Refresh, a working group it founded to promote artificial intelligence and machine learning in agriculture.

We know that the food we eat has a huge influence on our lives, but researchers are now saying that food might even change the way we speak. The birth of agriculture meant farmers could make softer food – think cheese and porridge – which affected the shape of our teeth and jaws, according to this new paper. As a result, people were better able to make the ‘f’ and ‘v’ sounds which started to spread along with agriculture.

US police seize huge haul of smuggled Chinese pork amid swine fever outbreak

On

Friday, US border police announced their biggest agricultural overhaul

seizure in the US: more than 1 million lbs of Chinese pork were found

being smuggled into the port of New York in Newark.

The

bust, which involved more than 100 customs and border protection

officials and dogs, found the meat hidden in 50 containers of food and

detergent products.

“The

pork was smuggled, from China, in various different ways including in

ramen noodle bowls to Tide detergent,” said Troy Miller, director of New

York field operations for the US customs and border protection.

The outbreak is alarming because it comes as China is battling with a deadly outbreak of African swine fever (ASF).

The

announcement comes as the oilseed and feed market speculates the size

of the impact of the current outbreak in China, home to half of the

world’s pigs.

Official

government figures show that at least 1 million pigs have been culled

in 115 outbreaks across the country since August last year.

But virtually no-one believes those figures, with most analysts claiming the figure is much higher.

Nor does the market believe that the disease is on the wane, despite the official figures showing exactly that.

Looking

at official reports from China’s ministry of agriculture shows that

there were five incidents in August, rising to 25 in September, hitting a

peak of 27 in October and falling away to just five incidents in

February.

On

Monday, the USDA said the size of China’s herd will fall 13% by the end

of the year, saying many outbreaks have not been reported because

provincial governments typically do not report the disease to the

federal government.

“Some

contacts have reported instances where individuals were actually

discouraged or prevented from publicizing outbreaks in their region… a

hog manager in Shandong Province was allegedly arrested for reporting

an ASF outbreak to the national government, after his reports to local

government were ignored,” the USDA said.

In

addition, the compensation paid to farmers is less than half the market

value of the pig, leaving many to cull pigs and sell the pork as

uncontaminated meat.

“At

this point, it is unclear when China’s government will have sufficient

control over the ASF situation to convince domestic industry to begin

restocking and expanding. Many in the swine industry are still taking a

wait-and-see approach to ASF in making business decisions,” the USDA

said.

Miller of US Customs and Border Protection said if the disease spreads to the United States, it could cause $10 billion worth of damage to the nation’s pork industry in just one year.

AgriCensus Prices Over 500 daily Spot Marker and Forward Curve price assessments for wheat, corn, soy, barley, vegoils, meals and seeds.

I have just finished reading The King of Oil by journalist Daniel Ammann, a book* that tells the story of the legendary and controversial trader Marc Rich, whom the FT once described as “one of the wealthiest and most powerful commodity traders that ever lived”. I would recommend the book to anyone that is interested in commodities.

Daniel Ammann writes,

Marc Rich, born Marcel Reich, the Jewish boy-refugee from Antwerp, barely escaped certain death in the Holocaust…Penniless and unable to speak a word of English, the young Reich fled (with his parents) to Morocco by freighter and, with a great deal of luck, finally reached the United States.

In 1954, at the age of 20, Marc Rich started in the mailroom at Philipp Brothers, at that time the world’s largest trader in raw materials. He worked his way up on to the trading floor in New York, before moving to head up the company’s Madrid office where he started trading oil. Some observers credit Marc Rich with inventing the spot crude market; previously all oil was traded on long-term fixed-price contracts. However, as Daniel Ammann writes,

“The notion of taking risks was as foreign to him as for the entire company, and this was reflected in Philipp Brothers German motto…” It is better to sleep well than to eat well”. The principle was drummed into employees that it was better to avoid a lucrative deal if the risks involved were high enough that they might endanger the entire company.

Marc Rich felt that Phibros was not aggressive enough. He left in 1974 to set up his own trading company, under his own name, in Zug Switzerland. He chose Switzerland because of the low tax rates and the fact that Switzerland was a neutral country; at that time, it was not even a member of the United Nations. As Marc Rich himself said, “The only bad thing about Zug is the fog.”

Marc Rich & Co was spectacularly profitable from the start, and by the end of the 1970s had thirty offices around the world. The five partners divided themselves between New York (where March Rich himself worked), London, Madrid and Zug.

In 1983, however, U.S. authorities charged Marc Rich with evading taxes and trading with Iran during the 1979/81 hostage crisis. Rich fled to Switzerland where he lived as a fugitive for 17 years.

Marc Rich admits buying oil from Iran during the embargo, as well as to supplying oil to apartheid South Africa and bribing officials in countries such as Nigeria. However, he argues that all this was legal at the time. For example, the bribing of foreign officials was legal in the United States until the passing of the Foreign and Corrupt Practices Act of 1977. In Switzerland, it remained legal until 2000. And as a non-US company based in Switzerland, Marc Rich & Co was legally (if perhaps not morally) exempt from the embargoes on Iran and apartheid South Africa.

Bill Clinton officially pardoned Marc Rich on the President’s last day in the White House in January 2001. The pardon was highly controversial, but, according to Daniel Ammann, it was the result of heavy lobbying by Israel. Throughout his career, Marc Rich had given large sums to the country, as well as working closely with Mossad, their security services.

For some, Marc Rich was,

“The capitalist without a country who makes deals with the enemy. The speculator who creates nothing of his own but only acts as an intermediary while profiting from others. The “bloodsucker of the Third World” as he was once referred to in the Swiss Parliament. The perfidious profiteer, who would rather leave his own country and give up his citizenship rather than pay taxes.”

But Ammann takes a more balanced view. He writes,

“Most commodities come from countries that are not beacons of democracy and human rights. The “resource curse” and “the paradox of plenty” are the terms economists and political scientists use to describe the fact that countries that are rich in oil, gas or metals are usually plagued by poverty, corruption, and misgovernment. If commodity traders want to be successful, they are forced—much like journalists or intelligence agents who will take their information from any source—to sit down with people that they would rather not have as friends, and they apparently have to resort to practices that are either frowned upon or downright illegal in other parts of the world.”

He adds,

“The commodity trade is a hard, capital-intensive business with tight margins. Profits of 2 to 3 per cent are considered quite satisfactory during normal times. It is only during unsteady times…that profits are significantly higher.”

The author describes an interview that he conducted with an ex-Marc Rich trader in a New York bar.

“Ethics,” he laughed. Then he pointed to my Diet Coke. “Your Coke can is made of aluminium. The bauxite that is needed to make it probably came from Guinea-Conakry. A terrible dictatorship, believe me,” he said. “The oil that is used to heat this room probably comes from Saudi Arabia. These good friends of the USA hack the hands off thieves just as they did in the Middle Ages. Your cell phone? Without coltan, there wouldn’t be any cell phones. Let’s not pretend. Coltan was used to finance the civil war in the Congo.” Do the people who criticise our work want to know any of this? Or would they rather just pick on us so that they can feel better about themselves”.

By the early 1990s, the legal case against Marc Rich was taking its toll. A difficult divorce and the death of his daughter added to his woes, and the partners began to worry about their company’s future. Marc’s legendry feel for the markets deserted him, as did many of his key traders. A failed attempt to corner the zinc market left the company with $172 million in losses and the firm was struggling. After at first resisting, Marc Rich finally sold his 51 per cent majority share in the company in a managerial buy-out for an eventual total of $600 million.

The first thing that the new owners did was to change the company name to Glencore. The company went public in May 2011 and now has a market capitalisation in excess of $42 billion.

Marc Rich himself died on 26th June 2013 at the age of 78. Despite his pardon, he never returned to the US.

But I leave the last word to Daniel Ammann,

“You must be a lucky man,” I said to the most successful and controversial commodities trader that the world has ever seen. Rich…remained silent for some time. Then, almost as if he were talking to himself, the King of Oil quietly replied, “Sometimes.”

Cargill will soon be opening a non-medicated premix production facility in Ohio, USA, as part of its efforts to find a solution to healthy livestock without antibiotics. The head of the group’s Premix and Nutrition business explained that nutrition was a key part in the transition away from drugs, adding that a healthier animal produced better meat and dairy. “Consumers really drive the supply chain,” he said, adding “The environment forces us to branch out far beyond just nutrients and ingredients.” Taking the move into ‘agtech’ one step further, Cargill has opened its first beauty lab in Shanghai, China, which will use the group’s expertise in food to develop sustainable and nature-derived products for the Asian market. In Russia, Cargill invested RUB 1.8 billion (USD 27 million) to expand the production of fats, oils and animal feeds in the Tula region as well as to set up a technology cluster.

Separately, Cargill has developed a new technology to give chocolate products the ‘right’ colour by using fewer chemicals, allowing to get previously difficult to obtain reddish and yellowish tones. The company explained that colour was very important for consumers and that this new method would make it much easier for food companies. Mondelez’ venture arm SnackFutures, meanwhile, has invested in a startup called Uplift which makes so-called “gut-healthy” foods and ingredients. Mondelez’ CEO said the aim was to re-invent snacks so that they have an active health component, “something that does not exist today.”

Olam reiterated its commitment to restore forests and fight deforestation as part of the Cocoa & Forests Initiative (CFI) across its supply chain, with a focus on West Africa. The company already used its supplier mapping to distribute 1.2 million trees in Cote d’Ivoire and Ghana. The aim is to “re-imagine the future of global agriculture where prosperous farmers (…) and healthy ecosystems can coexist,” the company said. The initiative fits well in the UN’s Decade on Ecosystem Restoration launched earlier this month. It hopes to restore 350 million ha of degraded land by 2030 to enhance food security and biodiversity.

In the same vein, China’s President said last week that he would not compromise the country’s health and environment for short term economic gain. The state market regulatory administration announced a new policy which made officials liable for issues around food safety, a major move to crackdown on the number of recent food scandals and improve the current food and drug safety standards.

The US’ Food and Drug Administration (FDA) and the US Department of Agriculture (USDA) announced they have finally agreed on a way to deal with cell-cultured meat. The FDA will regulate the collection and growth of cultured cells while the processing of those cells into meat, as well as labeling, will come under the USDA. While some wonder whether cell-cultured meat is commercially viable yet, some environmentalists have questioned whether the fuel used to power the labs is much better than the methane released by livestock. Regardless, the anti-meat trend seems to be getting increasingly popular. New York City’s mayor just announced “Meatless Mondays” for schools starting 2019/20. The program should reach out to almost a million students.

The US is set to get its first GMO seafood after the FDA gave AquaBounty the green light last week to start raising GMO salmon eggs in the country. The company, which is already implanted in Canada, had been blocked from the US market because of issues around labeling. The USDA’s bioengineered labeling guidance released in December will allow consumers to differentiate but opponents say the labels aren’t enough. AquaBounty’s CEO, on the other hand, pointed out that their salmon would be much fresher than the imported kind.

A study by the University of California found that fish stocks of the most commercially consumed fish had on average dropped by 4% between 1930-2010 but some areas, notably in the North Sea, had lost close to 30% of their stocks. Overfishing, warming temperatures and acidification of the ocean are to blame. The black sea bass in the Atlantic, however, seems to be thriving in the warmer water. In a bid to make fishing more sustainable, US group Bumble Bee Foods has tied up with a German technology company to launch a platform tracking yellowfin tuna using blockchain technology. Consumers will have access to the whole supply chain by scanning a QR code on the retail package and see for themselves that the products conform to the International Seafood Sustainability Foundation. Finally, winemakers are looking into replacing the traditional cylindrical glass bottles with Garçon Wines’ flat bottles made from recycled PET. The startup said that it can pack 10 bottles in the space of 4 traditionally sized bottled and that each bottle is 87% lighter, thereby reducing carbon emissions by 500g/bottle.

FACTBOX: What could be on China’s agriculture shopping list?

The US and China have for the past three months been locked in discussions about how to overcome a trade dispute that has slowed Chinese economic growth and seen the US-China trade balance slump to a record low last year.

Last month, Chinese imports from the US fell almost 20% compared to January, while its exports to the US fell 14.1%, indicating that the trade war is starting to bite almost a year on from when it started.

Over the weekend, Chinese officials from the ministry of commerce told journalists at an annual press conference they were working “day and night” to reach an agreement that would “remove all the tariffs imposed on each other” so that normal trade relations can resume.

So far much of the focus of the US administration has been on the so-called structural issues of intellectual property theft and an enforcement provision that China has refused to accept.

The main thrust from the US is how to address a trade balance with China that has ballooned from $268 billion a decade ago to a record $420 billion last year.

Bloomberg News last month reported China had pledged to buy an additional $30 billion worth of agricultural goods in an attempt to make a dent in to the trade balance and smooth the way for a trade deal.

The following is a factbox on what could be on China’s shopping list.

Soybeans

Soybeans is the jewel in the crown of US agricultural exports to China, although they have collapsed last year after China slapped a hefty 25% import tariff on US beans as part of the trade war.

Of $17 billion worth of US soybeans sold last year, China took just $3.1 billion, indicating that there is plenty of scope for this to increase by at least $10 billion to ensure exports returned to more historical 2016-2017 levels.

Any purchase above this would likely have to be done economically and come at the expense of Brazil – China’s biggest agricultural trading partner.

Wheat

The US has long since stopped being the marginal supplier of wheat to the world – losing that accolade to Russia.

Last year, the US exported $5.4 billion worth of wheat and just $100 million, or 400,000 mt, of that went to China, although that was particularly low last year.

US wheat sales to China have averaged around 1.5 million mt over the last five years.

If rumours that China could up that to as much as 7 million mt per prove correct, it would mean almost doubling its annual wheat imports but would still only make a $1.5bn dent in the trade deficit.

Corn/ethanol/DDGS

The US is a huge exporter of corn, selling 70 million mt or $12.5 billion of the grain on to the international markets last year.

However, China – itself a massive corn producer – has picked up just $50 million worth of that, raising expectations in the US that corn could be a big beneficiary of any trade deal.

However, ethanol and the animal feed Distiller’s grains (DDGS) would make for a more logical export target.

The US exports around $2.7 billion (6.5 billion litres) of ethanol each year with about 3% of that going to China.

It also exports around 12 million mt of DDGS each year worth around $2.5 billion.

In 2016 China took around 20% of that volume, but that has since collapsed to just 2%.

Ethanol probably makes the biggest sense, given China’s domestic target to blend 10% of the nation’s surging fuel demand with the alcohol.

While DDGS demand is likely to suffer in the wake of the African swine fever outbreak, China’s US ethanol imports have numbered over 200 million gallons in the past, a figure that could only increase as the E10 programme is rolled out more widely.

However, with China also intent on building its own domestic ethanol production capacity, any trade solution that includes ethanol exports could provide a short term fix and a longer term flashpoint.

Sorghum

The US exported around 4 million mt of sorghum, worth around $836 million last year and China took around 60% of this volume.

But the US has the potential to export double this volume.

In 2016, it exported 6.9 million mt worth $1.4 billion.

Meat

US exports of beef, pork and chicken totalled $18.2 billion last year, with beef accounting for $8 billion, pork $6 billion and chicken at $4.2 billion.

Of this, about $1.1 billion worth was exported to China, with beef exports amounting to $80 million, pork about $600 million and chicken $420 million.

However, with the ongoing outbreak of swine fever in China slashing the size of the hog herd there, most observers see a trade deal potentially triggering a huge rise in meat exports.

Sources in Spain and the US have already confirmed that Chinese buyers have been scoping the European and US market out for more pork imports as most analysts expect pork prices to soar in Q4.

Last week, Chinese forecasters JCI said they expected the size of the hog herd to fall by at least 10% – at least 40 million pigs, due to the infectious disease.

Commodity Conversation is proud to introduce a new weekly contributor: AgriCensus, a Price Reporting Agency (PRA) specialising in providing market moving news and benchmark prices for the bulk agriculture markets.

By Patrícia Luís-Manso – Head of Sugar and Biofuels Analytics at S&P Global Platts

Women are underrepresented in the commodity trading

business, in particular in sugar trading. Amongst the top trading houses that

control 85 percent of the total sugar traded in the world, less than 10 percent

of physical traders are women; and none of them holds a senior trading

leadership position. This has led to me to ask whether differences in the way

women and men develop and use their career networks could explain this

underrepresentation.

Networks are

essential to career development because they give access to information and

knowledge, as well as to decision makers, influence, endorsement and

reputation, emotional support and recognition.

Both male and female traders that I interviewed acknowledge that developing and nurturing career networks matter, and both invest in significant effort in doing so. Based on the interviews, I identified the structure of male and female traders’ networks and their networking behaviours. I concluded that career networks of men and women sugar traders are similar in terms of size and diversity. Moreover, female sugar traders tend to engage in networking behaviours to a similar extent (frequency) compared to their male colleagues.

However, they

differ in other aspects—ways that may be deterring women from accessing and

ascending in this profession. Key differences refer to the proportion of

high-status individuals and to the proportion of strong ties. Women sugar traders’ networks tend to have

less high-status individuals than men’s and to have a lower proportion of strong

ties.

Moreover, even

though female sugar traders engage to a similar extent as their male colleagues

in professional activities (conferences and seminars, for example), and in

community projects, other differences came to surface. First and foremost, female sugar traders engage in activities

that increase internal visibility less often than their male colleagues.

This could be going to lunch with their supervisor, or being on highly visible

committees at work. Instead, women tend to engage more often than their male

colleagues in maintaining contacts and socializing activities.

Based on these

findings, how can women close the wide gap in the trading profession? I

recommend three strategies.

STRATEGY ONE: Nurture strong ties to strategic partners.

Female sugar

traders’ networks have a smaller proportion of very strong ties compared to a

male network. In today’s highly connected world, weak ties may be less relevant

for career advancement.

The intensity of

the relationship with other individuals in the network does matter enormously

as a source of social capital. For career advancement, resources like

endorsements, validations and sponsorships that come from emotionally strong

ties may prove more effective for female career advancement than access to novel

information from weaker ties.

STRATEGY TWO: Participate more

in high-visibility activities.

Other studies have

highlighted the fact that women need high visibility to build legitimacy.

Excellent performance and solid human capital are necessary, yet not

sufficient, conditions for women to advance to managerial and leadership

positions.

STRATEGY THREE: Be more selective in terms of networking: quality over quantity.

Time is limited and women already engage in several networking behaviours. The key is to become more selective, and to think more about impact. This means that every time you participate in a network you should be prepare in advance to maximise impact.

Note: These findings are based on my final project presented as part of the Diploma in Organizational Leadership from the Saïd Business School at the University of Oxford (October 2018) The title of the assignment was Social capital and career development: is there a gender gap? Evidence from the Sugar Trading industry.

The biotech industry in the US is being proactive in its campaign to promote gene-edited crops as it hopes to avoid some of the consumer push back that followed the launch of GMOs. While GMOs involve adding foreign DNA to plants, gene-editing happens when DNA is removed. Nonetheless, groups like the Non-GMO Project say the two processes are almost identical and they predict that the industry will struggle to make gene-edited crops acceptable among the general public. The USDA is working to update its rules for gene-edited crops, while the head of the agency has repeatedly defended food companies against “fear your food” movements.

Unlike the USDA, however, the FDA currently classifies gene-edited food as drugs, which implies a very rigorous and lengthy approval process. This expert argues that this is a mistake as gene-edited food is still food but with a snippet of DNA removed. Gene-editing technologies such as CRISPR/Cas9 have huge potential in lowering carbon emissions or improving animal welfare but misguided and unjustified regulations will hinder their development and adoption, she argued.

Meanwhile, the FDA is considering a petition from the Swiss chocolate maker Barry Callebaut who is hoping to put health claims on its products. Although a similar petition was previously rejected, the European Commission authorised the health claims back in 2013. In its petition, Barry Callebaut pointed to some research which identified the flavanols present in cocoa as a promoter of healthy blood flow. Promoting the health aspects of chocolate could be essential to protect demand amid a general shift towards what the public perceives as healthier food.

In Belgium, Cargill announced its purchase of Smet, a family-owned producer of semi-finished chocolate products and gourmet chocolate. And while some are focusing on expanding their premium chocolate lines, Nestle unveiled its Cocoa & Forests Action Plan which will seek to remove all deforestation and labour abuse from its supply chain. As part of the effort, Nestle released the list of its suppliers in Ghana: Agroecom and Cocoa Merchants. It also revealed that Barry Callebaut, Cargill and Cocoanect acted as direct suppliers in Cote D’Ivoire. Another chocolate giant, Mondelez, made a similar pledge this week as it committed to monitor all of its suppliers in Ghana, Cote d’Ivoire and Indonesia with satellites to identify and address incidences of deforestation.

Such efforts could become essential, as a Senate committee in the US approved a bill that would force all large food retailers in Washington to publicly report any human right violations in their supply chain, in an effort to combat human trafficking and slavery. The food industry union argued against the proposal and said it would create a “paperwork nightmare”, while the dairy union said farmers and resellers should not be made responsible of regulating their suppliers. It highlighted that several government agencies already exist for that specific purpose.

Besides regulations, consumer demand is also forcing major food producers to adapt. Bloomberg compiled this list of ingredients which have been subject to sudden changes in perception, such as milk, cheese, sugar and corn syrup, and it noted that firms who failed to adapt have seen their value drop significantly.

Two major pharmaceutical companies, Sanofi and Novartis, announced that they have abandoned efforts to develop a drug to help obese patients lose weight. The decision was partly due to the difficulty in achieving significant results and the growing perception that obesity is not a disease but a lifestyle problem. On the other hand, Novo Nordisk, the last major firm researching the issue, is working on a new drug that could cut patients weight by up to 12.7%.

Lastly this week, researchers have finally solved one of the major mysteries in the food world: why do grapes catch fire when microwaved? Watch this video to understand the complexity of plasma clouds and microwave resonance, or just to see grapes exploding!

Australia inks trade deal with Indonesia to consolidate grain supply

The signing of the Indonesia-Australia Comprehensive Economic Partnership Agreement (IA-CEPA) on Monday in Jakarta is likely to consolidate Australia’s position as a principle grains supplier to one of the most populous nations on earth.

The deal was signed by Australia’s trade minister, Simon Birmingham, and his Indonesian opposite, Enggartiasto Lukita, and now heads back to the respective parliaments for final approval.

It comes after a drawn out negotiating process stretching back to 2010.

Indonesia is the second largest wheat importer in the world, and Australia’s biggest wheat customer, according to a report from Rabobank. Indonesia takes 20% of Australia’s exports with the free trade deal coming as trade relations between the government in Canberra and their counterparts in Beijing have deteriorated in recent months.

“Amidst global trade tensions and uncertainty regarding Australia’s barley trade with China, the signing of the… agreement in Jakarta yesterday is great news for Australian grains,” said Rabobank’s senior grains and oilseeds analyst Cheryl Kalisch Gordon.

The IA-CEPA agreement includes a 500,000 mt feed grain export quota for Australian feed wheat, barley and sorghum, which has the provision to grow unfettered by 5% per year and could prove to be valuable according to market sources.

“There won’t be a significant improvement (from the current arrangement), but if the Indonesian government moves to restrict feed wheat, then the allocation will be very valuable,” one Australia-based market source said.

Indonesia recently imposed a stringent phytosanitary regime on Ukrainian feed wheat imports, while Russian wheat has also fallen foul of the country’s standards.

But at the same time Indonesia has increased the wheat import from Argentina from 620,000 mt last year to 1.6 million mt this season, becoming the second biggest importer for that origin after Brazil, making harder competition for Australia.

Australia already has the option to export milling wheat into Indonesia at a zero duty rate, versus 5% imposed on other exporters, but Indonesia typically bans the import of barley, wheat and sorghum for feed purposes.

The agreement also makes provision for a joint grains market development initiative intended to develop the Indonesia-Australia supply route.

“These provisions offer important avenues to… compete more strongly with cheaper Black Sea or Argentinian origin wheat, which may have been used for feed (even though imported as milling),” Gordon said in an emailed statement.

While Indonesia hasn’t typically used sorghum or barley – the subject of China’s ire in its Australian anti-dumping investigation – in its feed mix, the agreement may encourage some outlet, according to the market source.

“Maybe it opens up Australia barley and sorghum into Indonesia when it prices competitively versus wheat into the feed ration,” the source said.

Finally, the agreement also includes eliminating tariffs on frozen beef, potentially boosting domestic Australian feed demand.

AgriCensus Prices Over 500 daily Spot Marker and Forward Curve price assessments for wheat, corn, soy, barley, vegoils, meals and seeds.

{kind=link}